Summaries like this, in your inbox every morning.

Sign up free →What happened: Micron Technology reports fiscal Q3 results on June 24 after market close. Analysts expect approximately $34.8 billion(約5.6兆円) in revenue and $19.72 earnings per share, representing 268% revenue growth and more than 930% earnings growth year-over-year. However, simply beating estimates may not be enough—investors are now demanding companies exceed current expectations and raise forward guidance.

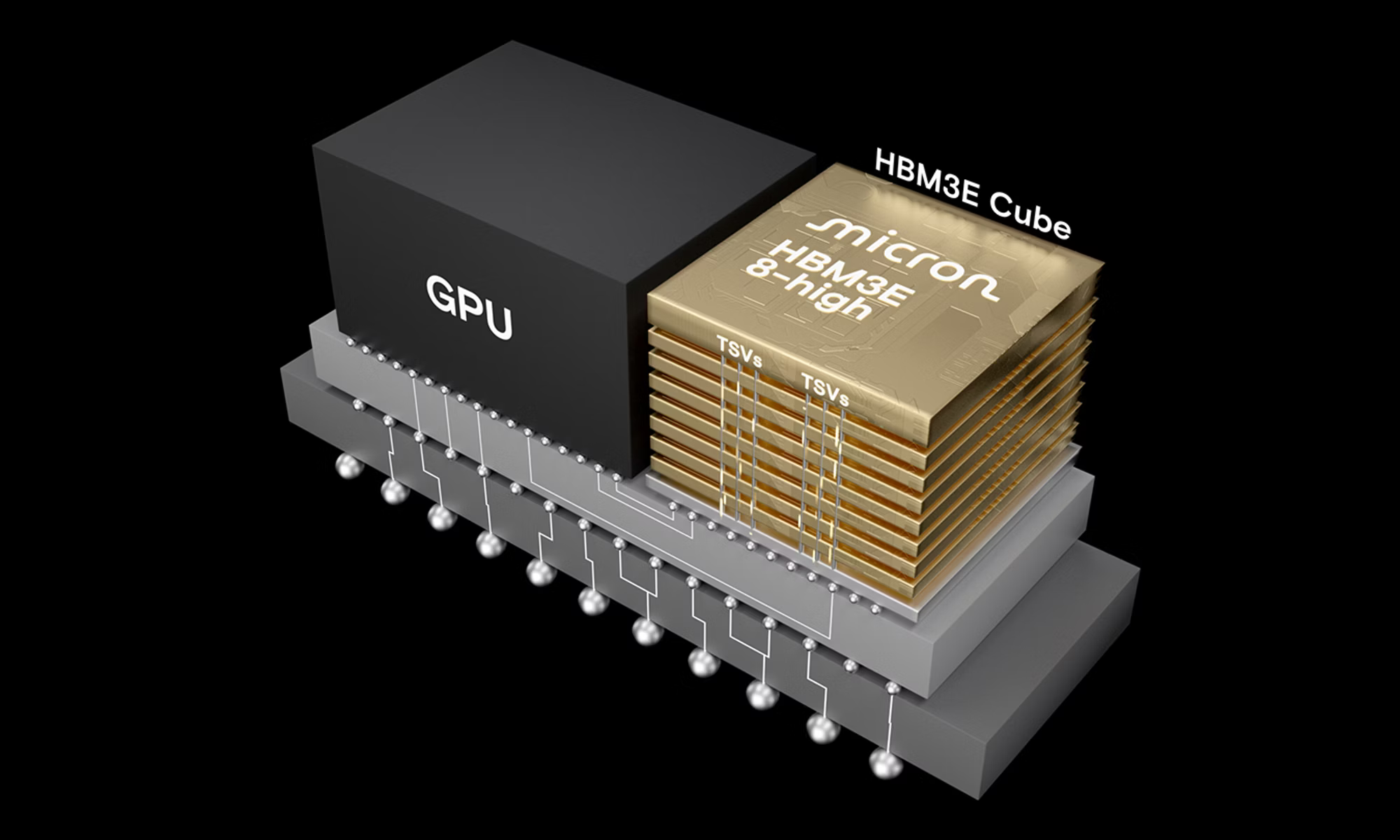

Why it matters: Micron's stock has risen roughly 830% over the last 12 months, driven by soaring demand for high-bandwidth memory (the advanced memory used alongside AI accelerators), tight global supply, and rising memory prices. With such a steep rally already priced in, the market has become unforgiving: ASML and Broadcom both faced sharp selloffs this year despite beating earnings because their guidance increases were deemed insufficient. Micron faces the same pressure to prove growth will accelerate further.

What to watch: To preserve stock momentum, management will likely need to exceed Q3 estimates, beat whisper numbers, and raise guidance for Q4 and beyond. Micron does carry one advantage over Broadcom: it trades for less than 10 times forward earnings and a minuscule PEG ratio of approximately 0.07—suggesting less of a valuation premium is already baked in. Industry leaders believe memory supply shortages could persist well into 2027, underpinning the long-term demand case.

No comments yet. Be the first to share your thoughts!

Log in to join the discussion

Get curated AI news from 200+ sources delivered daily to your inbox. Free to use.

Get Started FreeFree · takes 30 seconds · unsubscribe anytime

5 minutes a day. The AI essentials.

200+ sources · Email / LINE / Slack