Marketplace health insurance enrollment in the United States fell by 2.6 million people (from 21.8 million to 19.2 million) between February 2025 and February 2026, after pandemic-era federal subsidies that had capped monthly premiums expired at the end of 2025. The loss of those subsidies caused the average enrollee's cost for the same plan to jump about 114%, leading many to drop coverage. Health research shows that losing insurance coverage increases emergency room visits and hospitalizations for manageable conditions and worsens financial strain; even brief coverage gaps can cause lasting damage.

Summaries like this, in your inbox every morning.

Sign up free →What happened

Federal data released June 26, 2026, shows ACA marketplace enrollment fell from 21.8 million in February 2025 to 19.2 million in February 2026—a decline of 2.6 million people, or 12%, the steepest single-year drop since 2014. The drop followed the expiration of enhanced premium tax credits that had kept monthly payments low from 2021 through 2025; when they lapsed at the end of 2025, the average subsidized enrollee's cost jumped about 114%.

Why it matters

Research spanning decades shows that gaining health insurance coverage improves access to preventive care, reduces depression, nearly eliminates catastrophic medical bills, and can reduce mortality among older low-income adults by about 9%. Conversely, losing coverage makes care harder to get and afford, and even brief gaps can double emergency visits and hospitalizations in the first month for conditions manageable with regular care—such as diabetes complications, heart failure, and asthma.

What to watch

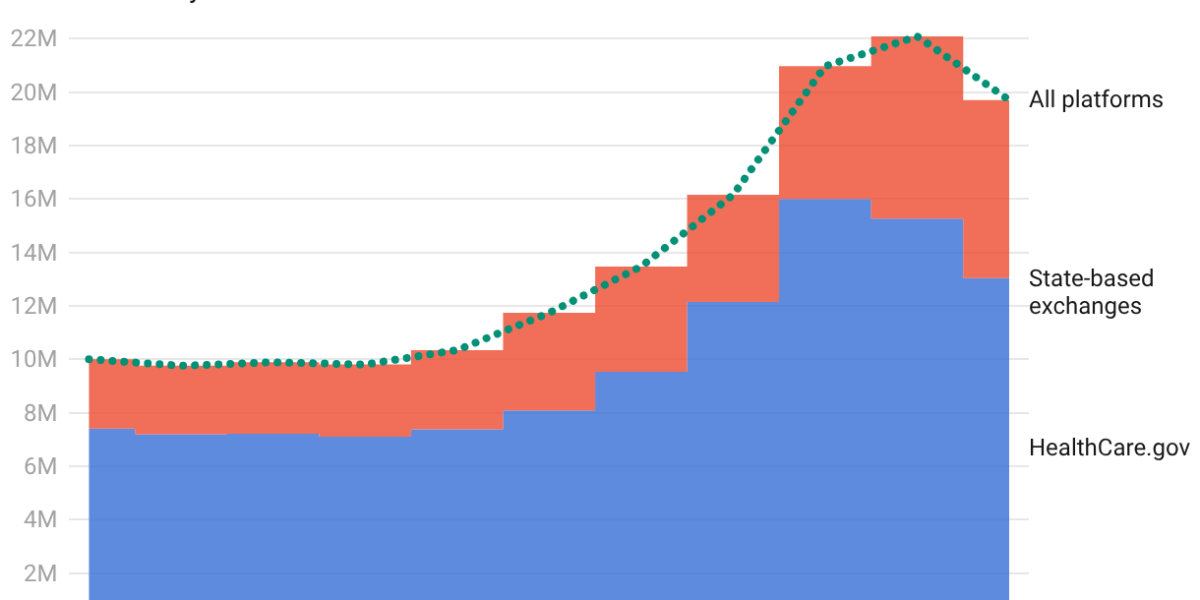

Health policy experts expect enrollment to decline further, to 16.5 million to 17.5 million by end of 2026. Insurers are requesting a typical premium increase of 14% for 2027, which would be the second year in a row with double-digit premium rises. The pattern also differed by state: HealthCare.gov (the federal enrollment website) saw an 18.7% average decline, while state-run exchanges saw only 6.3%.

On June 26, 2026, federal data revealed the sharpest single-year collapse in ACA marketplace enrollment since the exchanges opened in 2014. Marketplace enrollment fell from 21.8 million people in February 2025 to 19.2 million in February 2026—a loss of 2.6 million people, or 12%. The immediate cause was the expiration of the enhanced premium tax credits that Congress enacted during the COVID-19 pandemic to make ACA marketplace coverage more affordable. When these credits lapsed at the end of 2025, the cost shock was severe: the average subsidized enrollee's premium to keep the same plan jumped about 114%. Many people switched to cheaper, higher-deductible plans, but even those moves did not shield them from sticker shock—average premium payments rose 58% and deductibles climbed 37%, or more than US$1,000 per person.

The Trump administration offered a different explanation in a June 2026 federal brief, arguing that the subsidies had made some plans free, enabling brokers to sign people up improperly—including people who did not know they had been enrolled. The Centers for Medicare & Medicaid Services canceled 250,000 unauthorized enrollments and identified 200,000 unauthorized plan switches in 2025. However, independent analysts pointed to a simpler and more powerful explanation: when the extra subsidies ended, coverage became much more expensive, and many people dropped it or never paid their first premium. By February 2026, only 83% of people who had selected a marketplace plan had actually paid their premiums and kept coverage, down from 91% the previous year. The pattern of enrollment loss also differed sharply by geography: states using the federal HealthCare.gov enrollment website saw declines averaging 18.7%, while states operating their own exchanges experienced smaller drops averaging 6.3%, suggesting that state-run marketplaces had better tools to help consumers and provide additional financial assistance.

The health research cited by health economists studying this loss is sobering. Decades of research, including studies from the Oregon Health Insurance Experiment and analyses of Medicaid expansion states, show that gaining health insurance coverage improves access to preventive care, reduces depression, nearly eliminates catastrophic medical bills, and can reduce mortality among older low-income adults by about 9%. By contrast, losing coverage makes care harder to access and afford. When Tennessee dropped 170,000 adults from Medicaid in 2005, those who lost coverage were more likely to delay or skip care because of cost and reported worse health. A similar pattern emerged after pandemic-era Medicaid protections ended in 2023: in a survey of people dropped from the program, 3 in 4 worried about their physical health and 6 in 10 about their mental health, citing cost as the barrier to finding new coverage. Even brief coverage gaps are costly: among adults enrolled in Medicaid, emergency department visits and hospitalizations for conditions manageable with regular care—such as diabetes complications, heart failure, and asthma—more than doubled in the first month after a coverage gap.

Looking ahead, health policy experts expect enrollment to decline further, to between 16.5 million and 17.5 million by the end of 2026. Insurers selling ACA marketplace plans are requesting a typical premium increase of 14% for 2027, which would mark the second consecutive year of double-digit premium increases. The federal data released in June 2026 tracks enrollment only through February 2026, leaving unanswered questions about how many of the 2.6 million people who dropped coverage found alternative insurance and how many are now uninsured. The health consequences of this churn—the cycling in and out of insurance that many lower-income Americans experience—will take longer to measure, but past research offers a clear warning: when coverage disappears, the harm often emerges later in doctors' offices, emergency rooms, and family budgets.

The expiration of the enhanced premium tax credits—enacted during the COVID-19 pandemic to make marketplace coverage more affordable—is the direct cause of the enrollment collapse. These subsidies had more than doubled marketplace enrollment between 2020 and 2024, but when they ended on December 31, 2025, the financial burden on enrollees became unsustainable. While the Trump administration attributed some of the decline to improper enrollments (citing 250,000 unauthorized enrollments canceled and 200,000 unauthorized plan switches identified in 2025), independent analysts and the evidence point to price as the dominant factor: by February 2026, only 83% of people who selected a marketplace plan had actually paid their premiums and kept coverage, down from 91% the previous year.

The enrollment decline was not uniform across the country. States using the federal HealthCare.gov enrollment website saw an 18.7% average decline, while states running their own exchanges saw only a 6.3% decline—suggesting that state-run marketplaces had more capacity to help consumers compare plans and access additional financial assistance. Health policy experts now project enrollment to slide further to between 16.5 million and 17.5 million by the end of 2026, with insurers already requesting premium increases of 14% for 2027.

No comments yet. Be the first to share your thoughts!

Log in to join the discussion

Get curated AI news from 200+ sources delivered daily to your inbox. Free to use.

Get Started FreeFree · takes 30 seconds · unsubscribe anytime

1 minute a day. The AI essentials.

200+ sources · Email / LINE / Slack